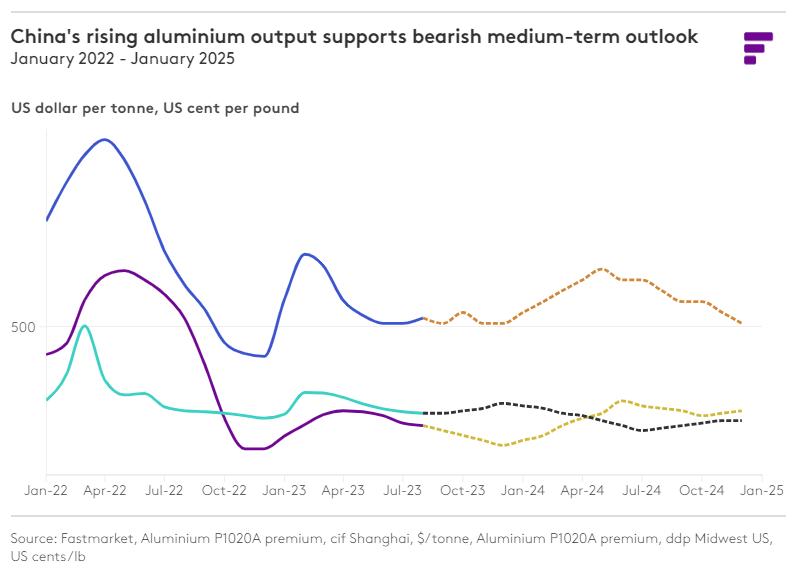

Rising supply headwinds for aluminium prices

The Chinese government is under immense pressure to support the country’s sluggish economic recovery. During a meeting of the 24-member Politburo of the ruling Chinese Communist Party, China’s top leaders signaled that more support is on the way to help its troubled real estate sector, boost consumption and resolve local government debt. But they fell short of unveiling the large-scale stimulus package that everyone has been waiting for. However, the prospect of rising metal supplies from China continues to act as a headwind to higher aluminium prices.

During the first half of 2023, China’s total primary aluminium production reached 20.16 million tonnes, a 3.4% increase compared to the corresponding period in 2022. Rising aluminium output from China supports our bearish medium-term bias on the light metal. Learn more.

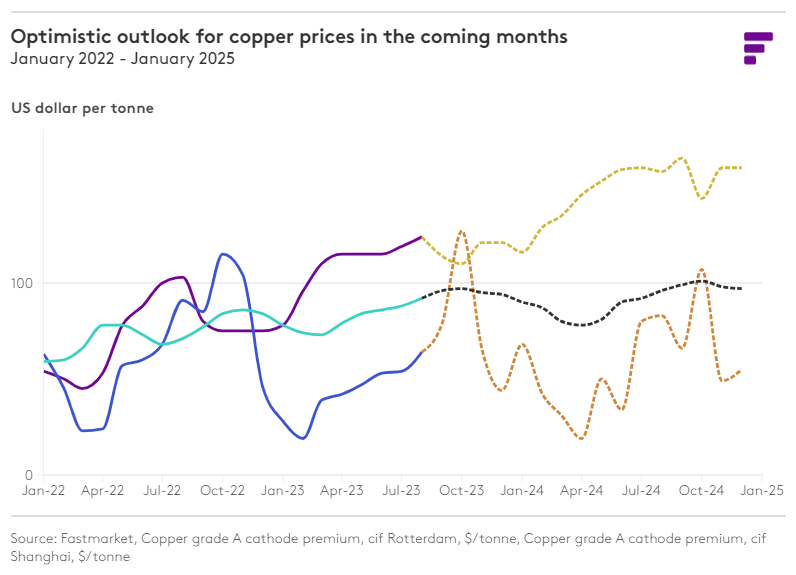

Positive stance unchanged for copper prices

We predict an optimistic outlook for copper prices in the coming months. Our price prediction is largely influenced by the anticipated weakening of the US dollar as the Federal Reserve’s rate hike cycle nears its conclusion. Coupled with this, we also see China’s growth accelerating, spurred by the implementation of additional stimulus measures. One of the stimulus measures being considered is lowering mortgage rates which should help to boost homebuying in the nation’s largest cities and ease fears in the property sector. We expect the outcome to be constructive for copper prices.

Interestingly, Comex’s speculative positioning being net short suggests that many investors might be caught off guard by a potential surge in copper prices. This misalignment provides an opportunity that astute investors could potentially exploit. Learn more.

Heatwaves potentially bullish for demand and lead prices

Overall, the global lead market looks balanced, so it is unsurprising that lead prices remain rangebound. But there are regional imbalances with the world ex-China showing a deficit and relying on exports from China. Recent developments, mainly China’s stimulus focused on the auto market and the heatwave hanging over large parts of the Northern Hemisphere and likely damaging lead-acid car batteries, are expected to be a bullish factor for lead demand.

Lead-acid batteries, especially older ones, tend to suffer in extreme weather conditions, whether it be cold or hot. Indeed, extreme heat tends to be a bigger problem than extreme cold. So, the heatwaves that are seeing extreme temperatures across large parts of the Northern Hemisphere are expected to result in a large number of battery failures, which will boost demand for replacement batteries. Learn more.

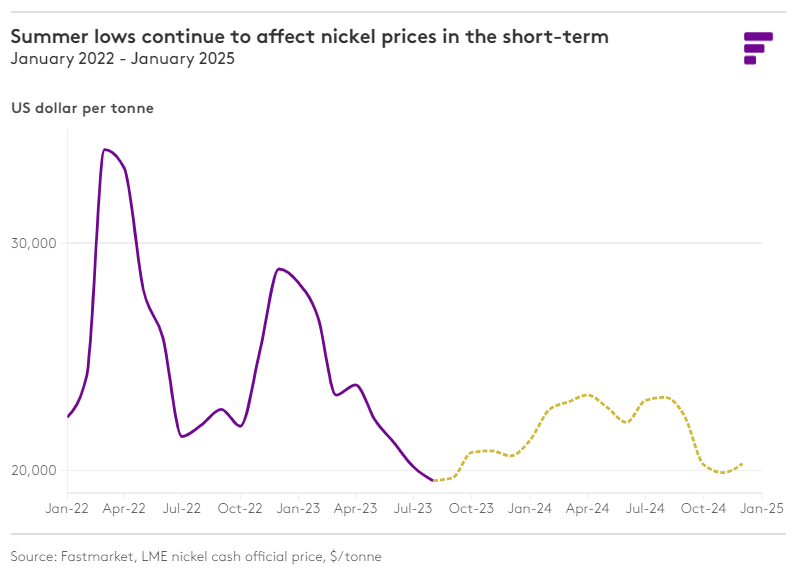

Nickel prices not out of the woods

While nickel has demonstrated some robust support in July, we still expect higher nickel prices in the medium-to-longer term. However, we are not convinced that the summer lows are behind us, as data warns that nickel demand may not benefit from the growing demand for Li-ion batteries in the biggest electric car market. The China Automotive Battery Innovation Alliance (CABIA) showed China’s preference for nickel-free lithium iron phosphate (LFP) batteries continued to grow, with the country’s output of these batteries rising by 11.64% month on month to 42.2-gigawatt hours (GWh).

Sharp upturn for tin prices in Q4

Despite recent sideways trading, tin prices are projected to exceed $30,000 per tonne in the coming months. This forecasted rise in tin prices is due to strong market resilience driven by a heavy backwardation in the LME tin market, the looming mining ban in Myanmar and the potential depletion of the currently ample Shanghai Futures Exchange’s tin stocks. A pronounced price escalation is likely, particularly if supply constraints persist and China’s economic growth accelerates in Q4 2023. Learn more.

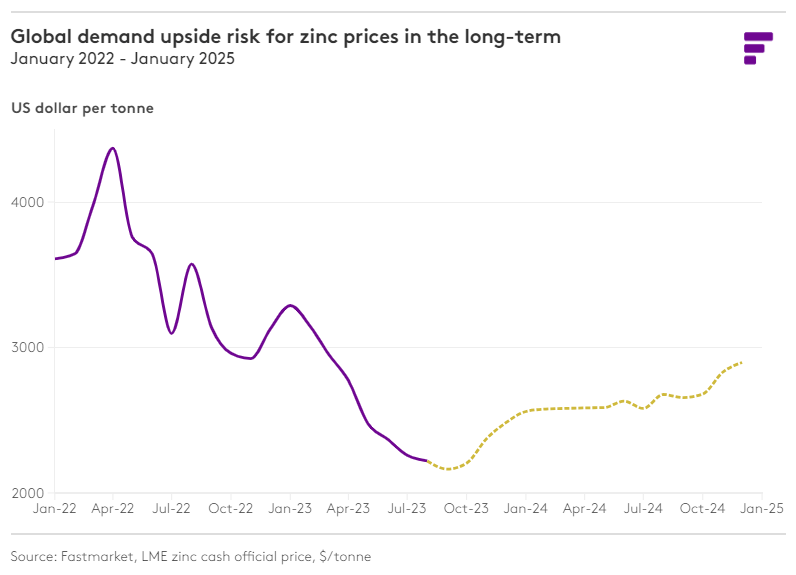

Fundamental revision reflects zinc price weakness

Accommodating for high utilization rates by Chinese smelters, we have cut our outlook for global demand growth to reflect slowing economic conditions. The net effect implies a 164,000-tonne surplus in 2023, compared with the 67,000-tonne deficit forecast previously. While our forecast implies the worst of the oversupply is weighted to H1 and may already be priced in, with a further annual surplus forecast for 2024, we see limited upside risk for zinc prices in the longer term. Learn more.

To understand the complex market conditions influencing price volatility, download our monthly base metals price forecast, including the latest base metals market outlook.