We interviewed Jordan Roberts, battery raw materials analyst at Fastmarkets, on current supply and demand gaps in the lithium market. He explains what this may mean for future prices, as well as how these supply deficits could potentially be fulfilled by unconventional resources entering the market.

Watch the video or read the summary with additional supply/demand balance and price charts below.

What are the limiting factors in new lithium supplies entering the market?

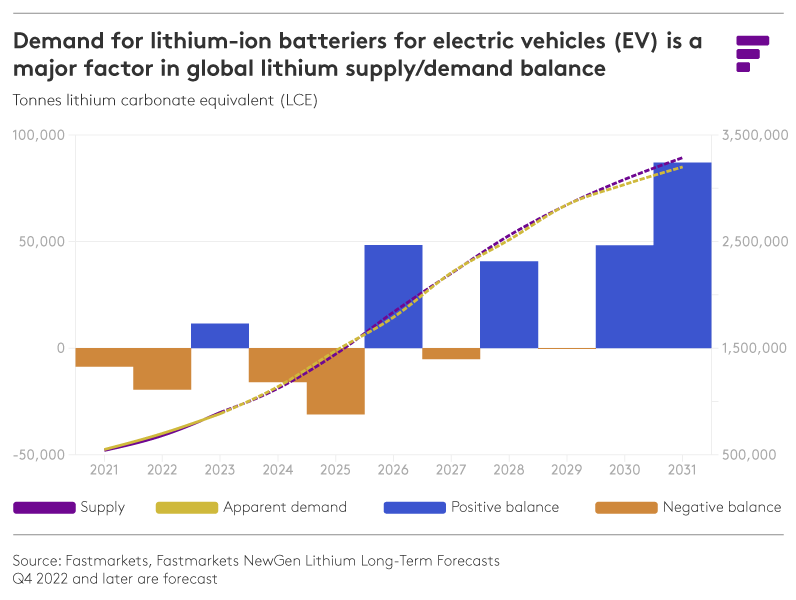

If we look at current capacity, upcoming projects and expansions, we predict significant growth in supply, but this is still expected to fall short of current demand for lithium-ion batteries for electric vehicles (EVs). Although we forecast periods of surplus this decade, the market will still be tight and consumers will likely take this as an opportunity to restock. Any surplus is relatively small in terms of the total market size and all it takes is one or two projects to be delayed to swing the balance to a deficit.

Although we forecast periods of surplus this decade, the market will still be tight and consumers will likely take this as an opportunity to restock. Any surplus is relatively small in terms of the total market size and all it takes is one or two projects to be delayed to swing the balance to a deficit.

There are plenty of projects in the pipeline, but the permitting requirements, regulations and the time these take to come online are some of the biggest problems facing the sector. Extracting lithium and producing a battery-grade product is complicated and the current development timelines we are seeing are not conducive to a move towards a balanced market. Without actionable policy and regulatory support, these timelines are only likely to lengthen due to increasingly stringent ESG parameters and lengthening permit processes. It is because of this that we expect the market to remain reasonably tight.

We are confident that new supply will come online to fill any large gaps but we think prices will remain elevated to incentivize this capacity. Timing will be important and if supply fails to expand at the necessary pace there will have to be some form of strategy change or demand destruction and this could constitute a move to smaller battery pack sizes or the penetration of more plug in hybrid electric vehicles as opposed to fully electric.

What unconventional lithium resources are currently available?

Unconventional resources include geothermal and oil field brines, as well as sea water. To a certain extent this also includes clay deposits, such as those located in the US and Mexico. Production from geothermal deposits could be the holy grail of sustainable lithium production, providing both clean energy and a source of lithium and these projects are located in Europe and the US. Oil field brines are a product of gas production and exploration, with wastewater potentially providing a resource. Parties are looking into seawater as, aside from the sheer quantities, seawater provides an evenly distributed lithium source and this would increase supply security, reducing the current chokehold Australia and Chile have on production.

As you would expect, like hard rock deposits, clay resources are higher grade than those sources previously mentioned. However, traditionally, the process of extracting lithium from clay is considered to be uneconomic. This is beginning to change but there are still risks associated with processing which involves techniques yet to be used on a commercial level.

Will these unconventional lithium resources close the supply/demand gap and how feasible are they?

We do expect some of these resources to contribute to supply within our long-term forecast, especially considering the investment and backing in several projects from OEMS and battery cell manufacturers. But the risk is to the downside and any delay in these projects coming online will lead to supply shortages.

Click here to find out more about the Fastmarkets NewGen Lithium Long-Term forecast

The real challenge with bringing this new supply online is that a lot of them rely on direct lithium extraction technologies, which have to be used because the grades in these resources are so low. Because of this we are already being conservative in our estimates, delaying projected timelines or ramp up schedules to take this risk into account.

Many of the assumptions used in these unconventional brine feasibility studies are said to be unrealistic or over-optimistic at best, especially considering a lot of these are still at the pre-commercial stage.

Keep up to date with the latest news and insights in the lithium market by visiting our dedicated lithium insights page.