The electric vehicle (EV) market – as markets tend to do – will find equilibrium. But right now. With demand exceeding supply, the path to equilibrium is most likely through constraining demand.

It is a path that will punish automakers that would face the loss of revenue, market share and brand equity. And at the heart of this supply and demand imbalance is the lack of battery raw materials (BRM).

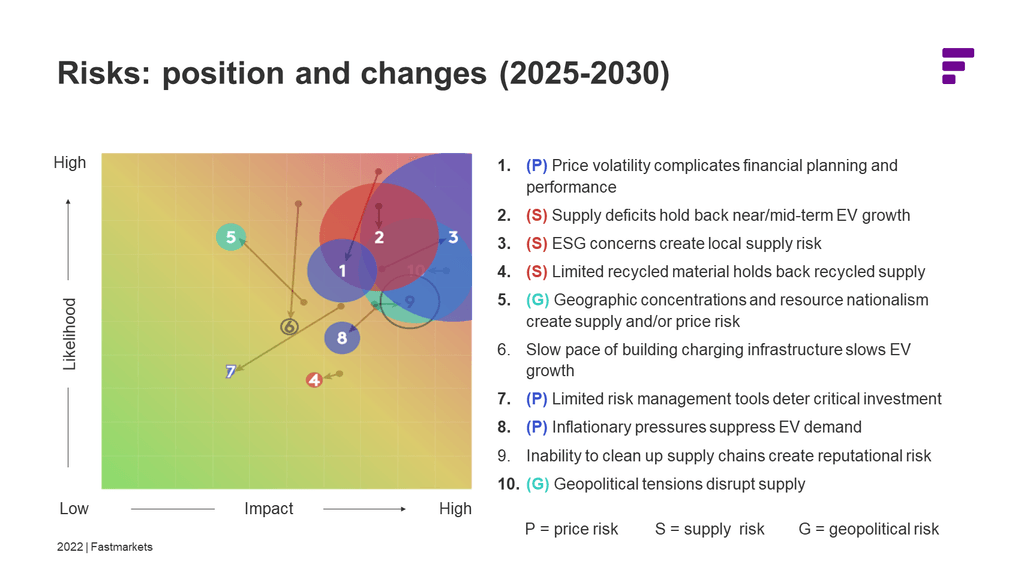

The Fastmarkets battery raw materials risk matrix gives automakers and battery makers a holistic, predictive, indexed view of risk in the 2022-2025 and 2025-2030 time frames. The matrix (above) shows all ten measured risks. But of the risks, three risk categories stand out:

The matrix (above) shows all ten measured risks. But of the risks, three risk categories stand out:

- Price risks that complicate the ability to build cars that are cost-comparative to internal combustion engine (ICE) vehicles or don’t cause automakers to make tough choices about margin or reducing costs elsewhere

- Supply risks across current, new and recycling supply sources, which will ultimately create winners and losers in the automotive space

- Geopolitical risks that complicate supply and price – making it harder to manage the next 10 years without likely disruptions.

Price risk: High price floors and greater impact of spot market prices complicates financial planning and performance

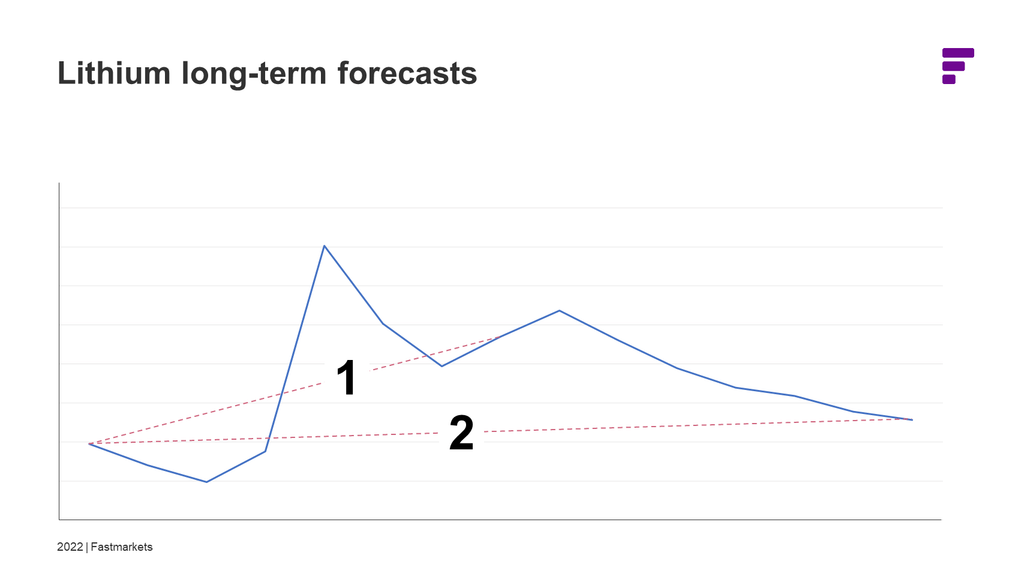

Prices initially soared in 2022 and then began to stabilize, albeit near record highs. Two factors weigh in the 2025-2030 period. First, a higher price floor has formed as demand places constant price pressure on supply.  For example, Fastmarkets’ lithium long-term price forecast shows:

For example, Fastmarkets’ lithium long-term price forecast shows:

1. Prices over 150% over 2021 prices in 2025 and over 45% over 2021 prices in 2032, impacting automaker margins; and

2. The spot market prices will have a greater impact on contract prices as producers move towards offering long-term contract tied to indexed prices, leading to greater cost basis volatility for automakers. Altogether, elevated BRM prices will affect all battery chemistries.

Supply risk: BRM supply deficits seem unavoidable, even with optimistic estimates

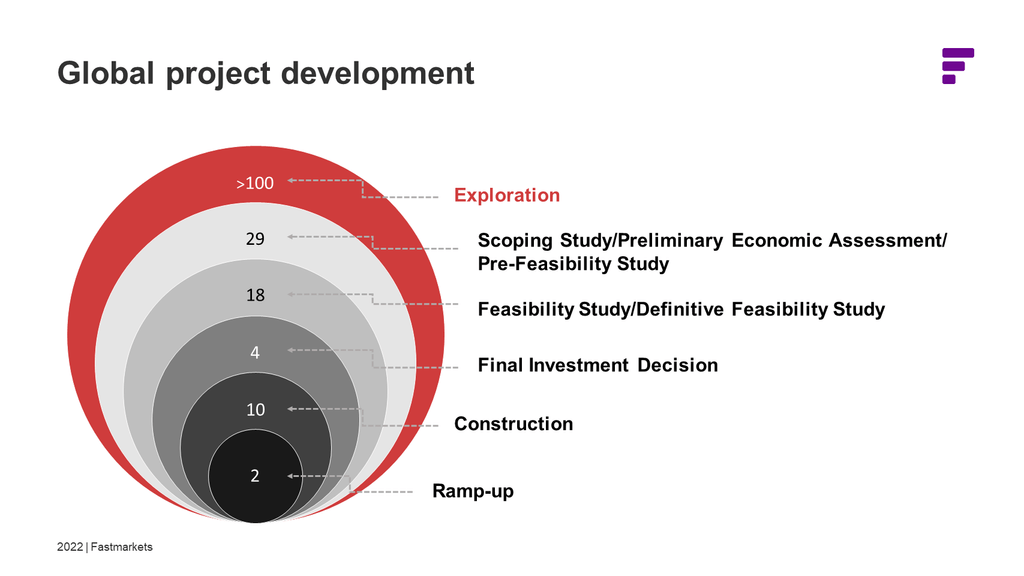

Current projects, new projects and recycling all have critical roles over the next 10 years. They all show promise and serve to lift supply – the overriding question is how much and how fast to feed increasing EV demand.

Deficits in current supply impact EV growth, particularly in the near-term

The good news is that current supply is growing as projects restart, expand, or improve yield narrowing the supply-demand imbalance. But that is a temporary reality; there is increasing clarity that supply won’t be in market fast enough or ultimately be sized to meet growing EV demand – even considering recessionary concerns.

The most acute risk exists in the next 5-7 years, or before enough supply from greenfield and recycling sources comes online.

ESG, technical and investment challenges limit and defer new supply, impacting EV growth in the mid-term

As we addressed at the Fastmarkets Lithium Supply & Battery Raw Materials 2022 conference in June, there are a large number of new projects in different stages of investment and development. Two issues come to the foreground. First, there is likely to be a material difference between theoretical supply and realized supply, particularly looking at the technical and investment issues associated with unconventional sources. The next issue is timing: how much and how fast?

The next issue is timing: how much and how fast?

Fastmarkets’ analysis shows that 63 of the currently planned new projects will produce usable supply before 2032; most will produce supply after 2032. Again, supply will come online, but it will persistently struggle to keep up with the pace of demand.

Limited material holds back recycling supply

Recycling technologies and markets are emerging that can make a difference, particularly towards the end of the 2025-2030 time frames. In this mix, the main source will come from manufacturing scrap; end-of-life scrap will likely play a larger role after 2030. The issue is how much of this material will become available and at what cost.

Fastmarkets forecasts that although available recycling scrap will grow 23.6% per year from 2021-2032, the actual recycled material will only represent 7.2% of overall supply in 2032.

Domestic and geopolitical realities are likely to complicate predictable supply

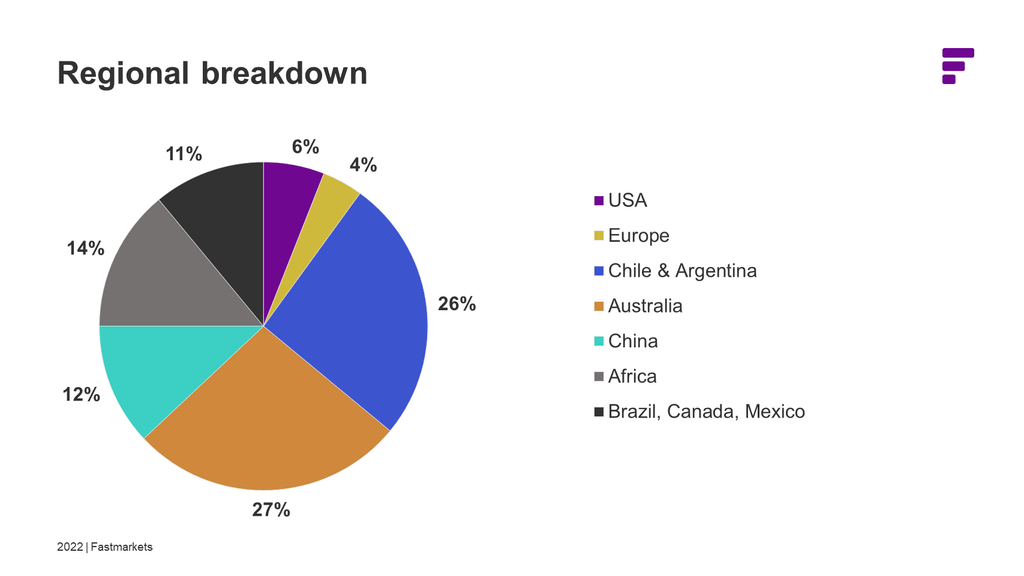

There are notable geographic concentrations in the lithium, cobalt and nickel markets. Concentrations where resource nationalism and geopolitical competitive interests play out.

Geographic concentrations combined with geopolitical realities complicate supply, especially for North America and Europe

Regional and national interest in materials like lithium simply does not match the political reality. China has gained a first-to-market advantage in treating BRM as a long-term economic strategy and domestic interests suggest a complex road ahead in the lithium triangle.

As we can see on the chart below, the near-term goal for North America and Europe may be to ensure viably growing EV and energy storage system (ESS) capacity. However, insufficient supply – where the US will produce 6% and Europe will produce 4% of the total global lithium production in 2032 – may complicate the ability to realize battery materials as a strategic achievement.

Geopolitical disruption is inevitable

As we are seeing in the Russian invasion of Ukraine, geopolitical realities can have a sizable impact on commodities. The challenge is the relationship between disruption potential and geographic concentration and how to create higher levels of resilience in the supply chains. Until this is worked out, automakers and battery makers are exposed to shocks to an already stressed system.

Achieving market equilibrium

Market equilibrium is inevitable; it may also be punitive. Constrained supply broadly equates to a loss of revenue opportunity and critical loss of market share and brand equity for some automakers. This compels virtually all of them to increase leverage in the supply chains as they internalize that batteries must be a core competency and critical operation.

Battery makers face the loss of revenue; but for some of the smaller players, a lack of supply endangers their very business.

The risk clouds have formed and seem to be growing in strength. Using the adage “to know the market you need to know the market”; clearly battery makers and automakers will need to rapidly increase their ability to understand and anticipate the markets and the risks that enable them to navigate the stormy waters ahead.