Traders across the global supply chain are looking to shore up availability as they consider the potential for sanctions on material from Russia to be ramped up rapidly, at the same time as Ukraine’s own ports and production have been choked and cut off by war.

This move to secure units and cover positions has led to events with few precedents. Nickel trading on the London Metal Exchange was suspended as the market traded at over $100,000 per tonne early on March 8 on short-covering, very low exchange stocks and fears about sanctions on nickel from Russia, which supplies about 10% of the world market for the alloying and battery material. (The last time such a suspension took place it was during the tin crisis in 1985-1986).

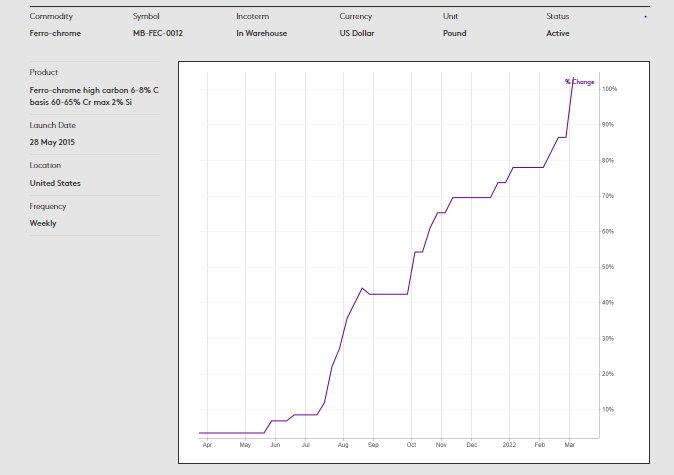

Even before trading was suspended the rise in nickel prices would have had a huge effect on the alloy surcharges that stainless steel mills use to pass on raw material costs to their customers. (In the US high-carbon ferro-chrome prices are also trading at or near all-time highs). And companies downstream in the battery sector, including OEM and auto-firm purchasing teams, will be looking on queasily at the volatility in this critical material.

Such high and volatile prices suppress and destroy demand, of course. A week ago, remember, nickel was trading at around $25,000 per tonne.

Such high and volatile prices suppress and destroy demand, of course. A week ago, remember, nickel was trading at around $25,000 per tonne.

Notwithstanding the marginal moves that have been made in some markets to shorten and secure supply chains in the wake of Covid, the effects of the Russian invasion are being felt in markets well beyond nickel.

Consider the US steel mills that look likely to have to pay over $100 per ton more for prime scrap in March as availability of iron units from Russia and Ukraine ceases, and the price rises that they are therefore proposing themselves. Or the rolling mills in Europe that turn slab and billet imports from Ukraine and Russia into hot-rolled coil and rebar and must now source feed elsewhere.

Here’s just a small selection of this week’s headlines, showing the breadth and depth of the impact of the conflict. (Subscribers only. Scroll to the bottom of this article to access free content.)

- Supply crimp sends pig iron prices on wild run

- US HRC index tops $54/cwt in volatile mart

- EU HRC sellers hold back from trading, sentiment bullish

- Alcoa to stop buying from, selling to Russia, CEO says

- Rusal halts alumina production in Ukraine

The interconnectedness of the supply chain can be seen through the effects of this conflict on Russia-based aluminium producer Rusal, which has had to shut the Ukrainian alumina refineries that typically feed its Russian aluminium smelters. Corporates are imposing informal sanctions themselves on trading with Russia even without such moves being mandated by governments, banks will not finance trade and the country has been cut off from the SWIFT network: little wonder then that consumers in Europe and the US have driven prices and premiums for aluminium to all-time highs.

Longer term, and failing a speedy resolution to this crisis, it would be reasonable to speculate that more material from Russia, a large commodity producer, would flow towards China, a large commodity consumer. This is not to say that global supply balances will change in the medium term, but traders outside China should be considering what this means to their business. Once such flows are established they do not readily shift.

Last, and by no means least, I should note that this short commentary rests squarely on the far more substantial work of my colleagues in Fastmarkets, and particularly those in our team in Ukraine.